Universal Mobile Payment System Enables Secure Transactions Across Any App or Platform

Invented by WANG; Justin

Mobile payments are now a part of daily life, but anyone who has tried to pay with their phone while traveling or shopping at different stores knows the pain of incompatible payment codes and apps. The patent application we will explore today brings a fresh solution: a universal mobile payment method and system that works across all platforms—even those not in partnership. Let’s unpack the story behind this invention, the science that makes it possible, and why it could change how we all pay.

Background and Market Context

Mobile payments are everywhere. In coffee shops, buses, supermarkets, and even at small street vendors, you see folks tapping phones, scanning codes, or holding up smartwatches to pay. But behind this convenience lies a tangled web of apps, codes, and partnerships that can turn a simple transaction into a headache.

Let’s say you’re at a store that only accepts one payment app, but your phone uses another. You want to pay with your phone, but the QR code at the counter only “speaks” to their app. You either need to install their app, sign up, maybe even set up a new account—or just give up and use cash. For shop owners, the situation isn’t much better. They might have to juggle several payment platforms, each with its own QR codes, fees, and management tools. Keeping customers happy and the cash flowing can mean signing up with a dozen different payment companies, printing out lots of codes, and making sure staff know how to work each system.

The problem grows when you travel. Maybe your American payment app doesn’t work at a shop in Japan. Or the shop uses a local payment code you’ve never seen. Even if both the shopper and the store want to use mobile payment, the transaction just won’t happen if the systems don’t match.

This is not a small issue. The mobile payment world is booming, with dozens of services: Apple Pay, Google Pay, PayPal, TW Pay, Line Pay, Fami Pay, PX Pay, JKO Pay, and many more. Each wants to be the go-to payment app, but with so much choice comes confusion. For users, keeping up with all these apps and codes is tough. For businesses, supporting every customer is almost impossible.

What if you could have just one app that could pay anywhere, no matter what code the store uses? What if you could pay even when the payment code and your app have never “met” before? That’s the heart of this new invention.

The patent application introduces a system and method that lets you use one mobile payment app—a universal payment app—to pay at any store, even if their code was made for a different system. It doesn’t matter if your app and their payment code have a prior agreement or not. The universal app bridges the gap, so you can pay smoothly, and stores can accept any customer. This is a big promise, and if done right, could clear away much of the friction in today’s busy, app-filled payment world.

Scientific Rationale and Prior Art

To understand what makes this new method different, we should first look at how mobile payments usually work. In most cases, a payment code—like a barcode or QR code—is made by a payment platform (let’s call it Platform A), and only the matching app (App A) can read and process it. If you try to use App B on the same code, it won’t work. That’s because the code and the app share a special “language” or protocol. In some cases, two payment providers make an agreement, so App B can also read codes from Platform A. But if there’s no agreement, App B is left in the dark.

This system design is intentional—it keeps platforms “sticky” and encourages users to download specific apps. But it creates roadblocks for users and businesses. The more payment platforms there are, the more codes and apps you need.

There have been attempts to create “multi-platform” payment apps—apps that can read codes from more than one provider. Some big payment companies have made deals to allow their apps to accept each other’s codes. Others rely on the user to select the right app or switch between apps on their phone. But these solutions rely on pre-arranged deals or require the user to do extra steps. None of them truly let a single app pay at any code, anywhere, even with no prior agreement.

The heart of the problem is code recognition. Payment codes are usually tied to a specific app or system. If an app doesn’t know how to read a code’s structure or doesn’t have a business deal with the code’s provider, it can’t process the payment. Some apps try to “guess” the code’s content, but this is usually blocked for security and privacy reasons.

Previous inventions in the space have focused on:

- Creating shared payment networks where all members agree to common code formats.

- Allowing users to select the right payment app when scanning a code.

- Using NFC (near-field communication) as a backup when codes don’t work.

- Having stores print multiple codes for different platforms.

These solutions all require either prior agreements, more work for users and stores, or both. None truly solve the “universal app for all codes” challenge, especially when the payment code and the app don’t know each other at all.

What’s new about this patent? The universal payment app in this invention doesn’t need to recognize or “understand” every payment code. Instead, it has a way to handle even unknown codes by offering a “financial transaction trigger”—a link or button that lets the user complete the payment through other means, like a credit card or bank transfer, right inside the universal app. The app can also link out to other payment platforms as needed. This means, even if the code is from a platform the app has no relationship with, the payment can still go through smoothly.

By focusing on offering flexible payment triggers and connecting to standard financial rails (like card payments and bank transfers), the universal app can work with any code—no need for advance agreements or partnerships. This approach is a big shift from the “closed garden” model used by most current payment systems.

Invention Description and Key Innovations

Let’s walk through how this universal mobile payment method and system actually work, and highlight the new ideas that set it apart.

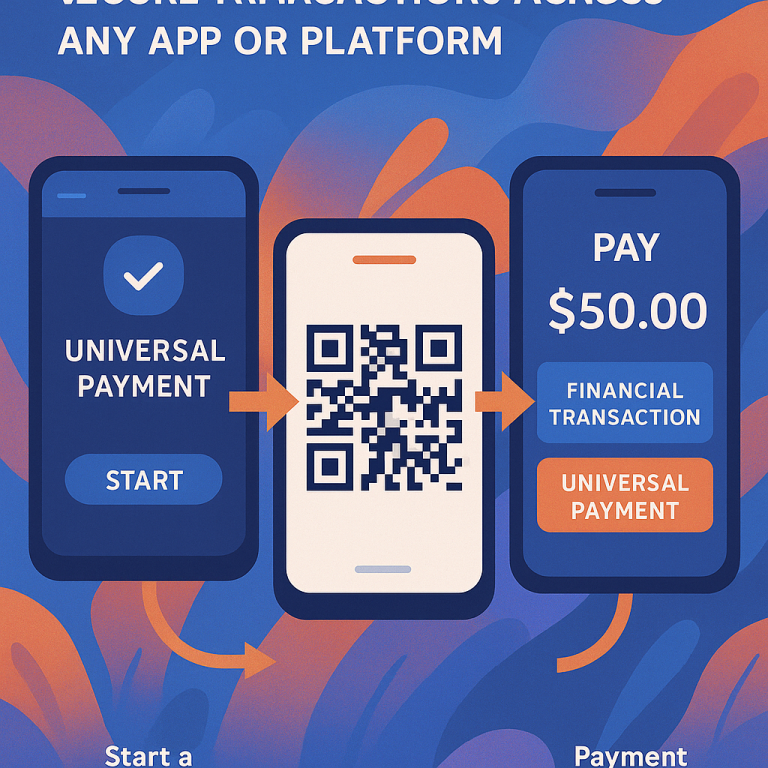

The core of the invention is a universal payment app—a single app installed on your phone or device. Here’s what happens when you go to pay:

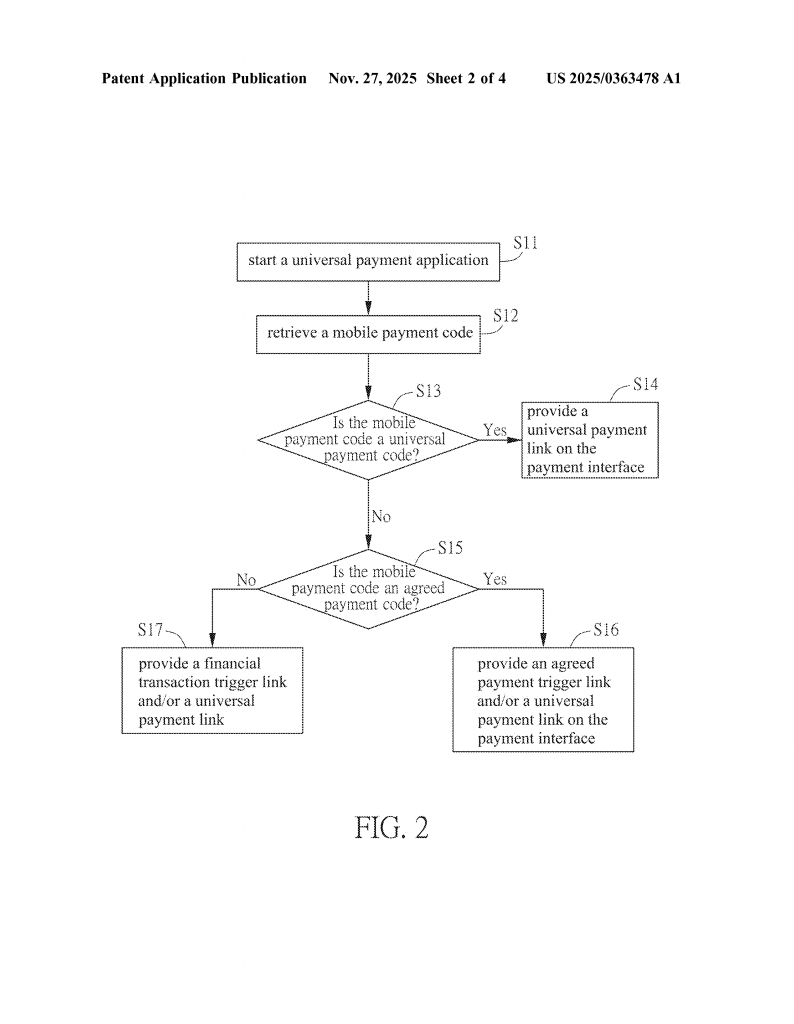

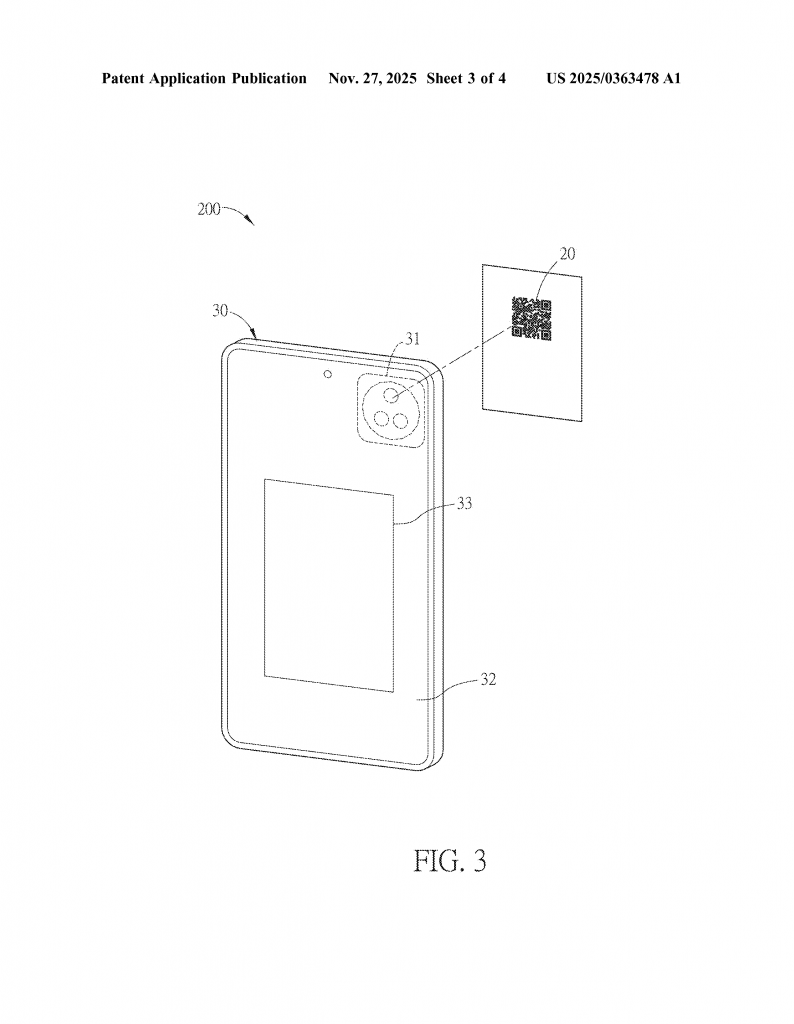

You start the universal payment app, just like opening any payment app. Then, you scan the store’s payment code. This could be a barcode or QR code, and you can capture it with your phone’s camera or by using wireless communication like NFC.

The universal app checks the code. There are three types of codes it may see:

- Universal payment code: Made for the universal app itself.

-

Agreed payment code: Made by another payment platform, but the universal app can recognize it because of a prior deal.

- Non-agreed payment code: Made by another payment platform, and the universal app has no way to “read” or recognize it.

If the code is universal or agreed, the app can process it as usual, either directly or by linking to the right partner app. But the real magic happens with non-agreed payment codes. When the universal app scans a code it doesn’t recognize, it still gives you a payment interface with special options:

You see a “financial transaction trigger link” and/or a “universal payment link.” The financial transaction trigger lets you pay using your credit card, debit card, prepaid card, or by bank transfer. The universal payment link may try to pay through the universal platform if that’s possible.

This means, even if your app doesn’t “know” the code, you can still pay right away. The app can handle the payment through your bank or card provider or connect you to another payment platform if needed. You don’t need to install another app, set up a new account, or worry about the code’s origin.

For the store, nothing changes. They just display their usual QR code or barcode. For the user, it’s seamless—just scan and pay, no matter the code’s source.

The invention also works with codes sent through NFC or other wireless methods, so it’s not limited to printed or displayed codes.

Let’s look at an example. Imagine you’re traveling and go into a shop that only uses a local payment app. Their QR code is a “non-agreed” code for your universal app. Normally, you’d be stuck. But with this system, you scan the code, and your app gives you the option to pay with your credit card or bank account. The universal app handles the rest, connecting through the right financial networks to complete the payment for you and the store. Everyone is happy, and no sale is lost.

The patent application also goes further. It describes a complete payment system, including the mobile payment code (assigned to the store) and the electronic device (assigned to the shopper) running the universal app. The system can handle codes in many forms—barcodes, QR codes, NFC signals—and provides the flexible payment options described above.

Key innovations in this invention include:

- Allowing a single payment app to process or route payments for any code, regardless of prior agreements.

- Offering financial transaction links (like card payments or bank transfers) as a fallback when the code cannot be recognized.

- Providing a unified payment interface that adapts based on the type of code scanned.

- Reducing the need for users to install multiple payment apps or for stores to display multiple codes.

- Enabling cross-border and cross-platform payments with minimal set-up.

This approach simplifies the lives of both shoppers and stores. For users, it means one app, fewer headaches, and more freedom to pay however and wherever they want. For stores, it means less need to manage many payment platforms and a greater chance of completing more sales, even with travelers or visitors using unfamiliar payment systems.

Conclusion

The universal mobile payment method and system described in this patent application tackles a real and growing problem in our modern payment landscape: too many apps, too many codes, and too many barriers to simple transactions. By giving users a single app that can pay anywhere, regardless of the code’s origin, and by using smart triggers to handle even unknown codes, this invention promises smoother payments for everyone.

It’s a big step toward a world where your phone or device can handle any payment situation, at home or abroad, with less hassle and more reliability. As mobile payments continue to grow, solutions like this are not just helpful—they’re necessary to keep up with the pace of global commerce. If you’re a business leader, retailer, or traveler, this universal approach to mobile payments could soon make your life a lot easier.

The future of payments is simple, flexible, and open to all. This patent shows us how we might get there.

Click here https://ppubs.uspto.gov/pubwebapp/ and search 20250363478.