Safeguard Digital Payments: New System Verifies Transactions and Blocks Fraud in Real Time

Invented by SZMIGIELSKI; Albert, YARNOLD; Adam

Let’s jump right in. Every day, people and businesses use checks, transfers, and digital payments. But what happens when someone tries to cheat the system? That’s where this new patent application comes in. It’s all about keeping your money safe by making sure payment instruments—like checks and digital drafts—are real and trustworthy. We’ll walk you through the market setting, the science behind it, and the special ideas that make this invention stand out.

Background and Market Context

Imagine you get a check from someone. You want to cash it, but how do you know it’s real? In today’s world, fraud is a big problem. Checks are copied or changed. Digital payments can be faked. And when banks process payments, they can’t always tell right away if something is wrong. It might take days before anyone notices a fake check or a stolen account number. That’s risky—for both people and banks.

Payments today come in many forms. There are paper checks, electronic checks, wire transfers, and new digital tools like digital negotiable instruments. Each way of paying has its own weak spots. With checks, someone might copy a real check or change the amount. With digital payments, hackers might break in or trick people into sending money. Every day, banks and businesses lose a lot of money to these tricks. When fraud happens, people lose trust in the payment system. They worry about getting paid or paying someone else.

Banks use different steps to stop fraud. They check names, addresses, account numbers, and signatures. Sometimes they look at the paper the check is printed on or use special ink. But clever criminals can get around these checks. Sometimes, even bank workers can’t tell if a check is fake. And with digital payments, the risk is even higher. Hackers can steal private details or copy digital signatures. This problem is getting worse as payments move faster and more online.

Right now, the process of checking if a payment is real isn’t fast enough. It often takes hours, days, or even weeks to find out if a check is bad or a payment is fake. That’s way too slow. In the meantime, banks might give out money that isn’t really there. This makes businesses and people worry every time they get paid. Everyone wants a way to know, right away, if a payment is safe and real.

This is why there’s a need for a better system. One that can check payments quickly, stop fraud before money moves, and give everyone peace of mind. This patent application introduces a new way—using a smart, fast, and secure engine to check every payment instrument. It’s designed to help banks, businesses, and people trust each transaction. Let’s see how the science works and what makes this solution different from what’s out there now.

Scientific Rationale and Prior Art

How do you check if a payment is real? In the past, banks checked paper checks by hand. They looked at the name, address, and signature. Later, computers helped by checking account numbers or running information through databases. For digital payments, banks used passwords, digital signatures, and sometimes special chips or codes. But each of these methods has limits.

Fraudsters use advanced tricks. They can copy checks exactly or use stolen details to make digital payments look normal. They might even use special printers or software to change what’s on a check or payment file. Sometimes, criminals pretend to be someone else to trick banks and businesses. Because old systems check only a few things—like a name, number, or signature—they can miss clever fakes.

One tool that helps is a hash function. A hash function takes information (like the details on a check) and turns it into a unique, scrambled code—a “hash.” If you change even one letter or number, the hash changes completely. This makes hashes good for checking if something is exactly the same as before. Banks and tech companies use hashes to check files, passwords, and sometimes payment details. But hashes alone aren’t perfect. If someone knows how the hash works and has the same details, they can make a matching hash. So, to make things safer, systems add extra steps, like using secret keys or combining hashes with private information.

Another idea is using databases. Databases store lots of information—like every check a bank has seen. When a new payment comes in, the system checks the details against the database. If everything matches, the payment is likely real. If something’s off, the system can flag it for review. But searching big databases can be slow if not done right. And if fraudsters get into the database, they might change or steal information.

Some newer systems use blockchain or distributed ledgers. These are special databases that are shared and copied in many places at once. When a payment is added, it’s written in a way that can’t be easily changed. This makes it hard for criminals to fake or copy payments. But blockchain systems can be slow or hard to connect with older banks and payment tools. Plus, not everyone is ready to use blockchain yet.

In summary, the tools we have—hashes, databases, signatures, and even blockchain—each help stop fraud. But they aren’t perfect alone. Criminals keep finding new ways to trick the system. There’s a need for smarter, faster ways to check if a payment is truly real. The invention in this patent application brings these ideas together, making them work smarter and faster to protect your money.

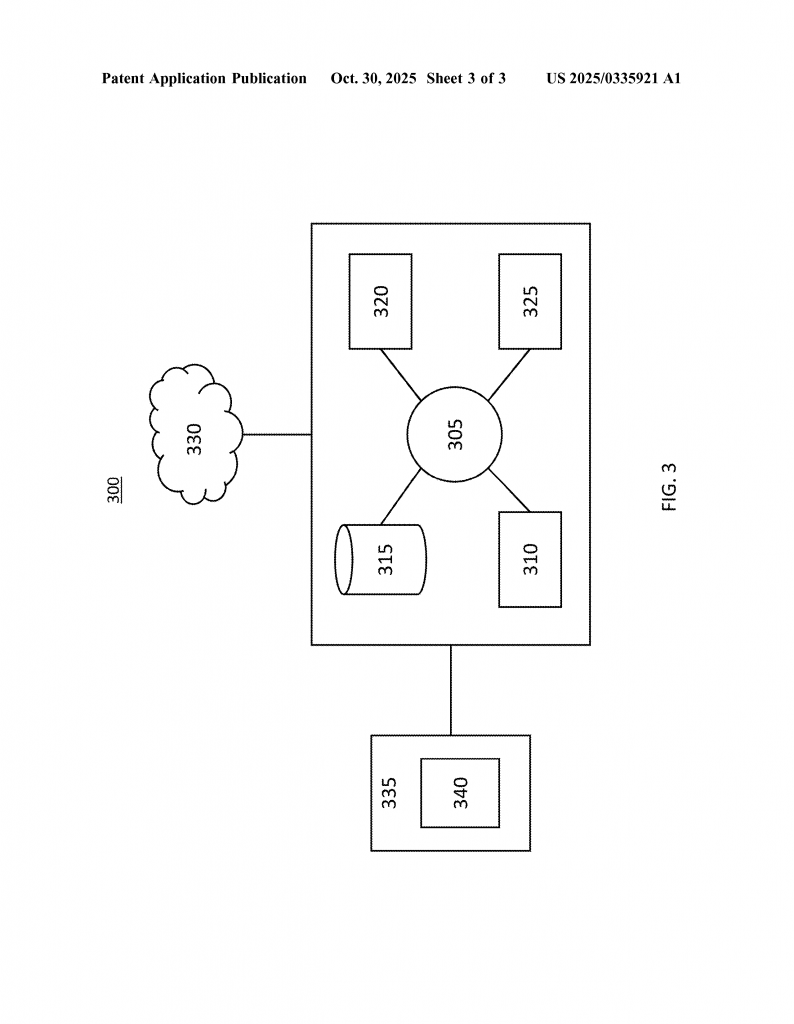

Invention Description and Key Innovations

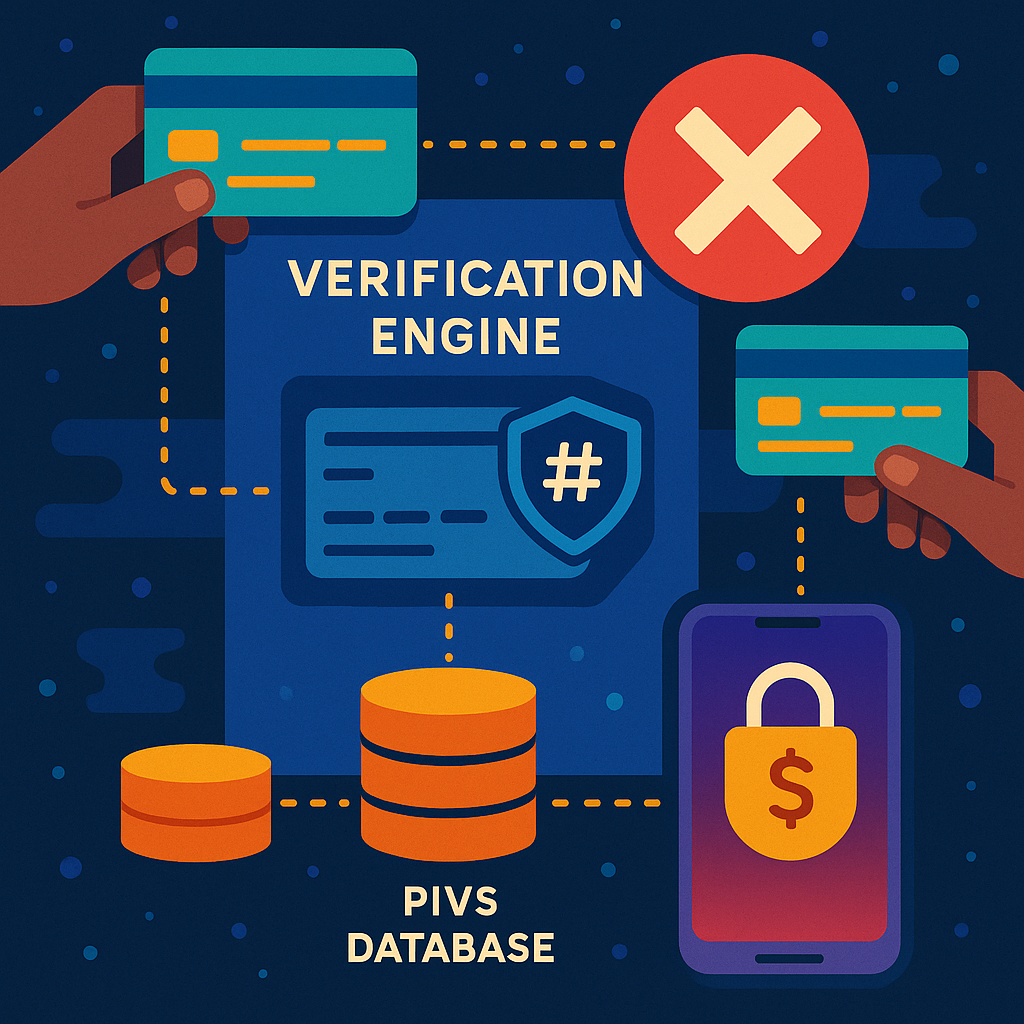

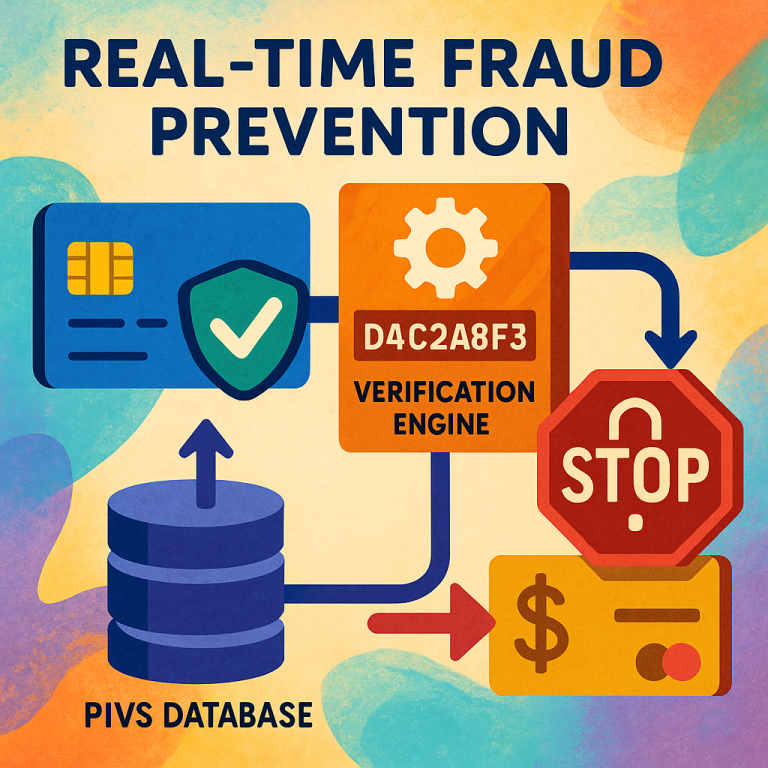

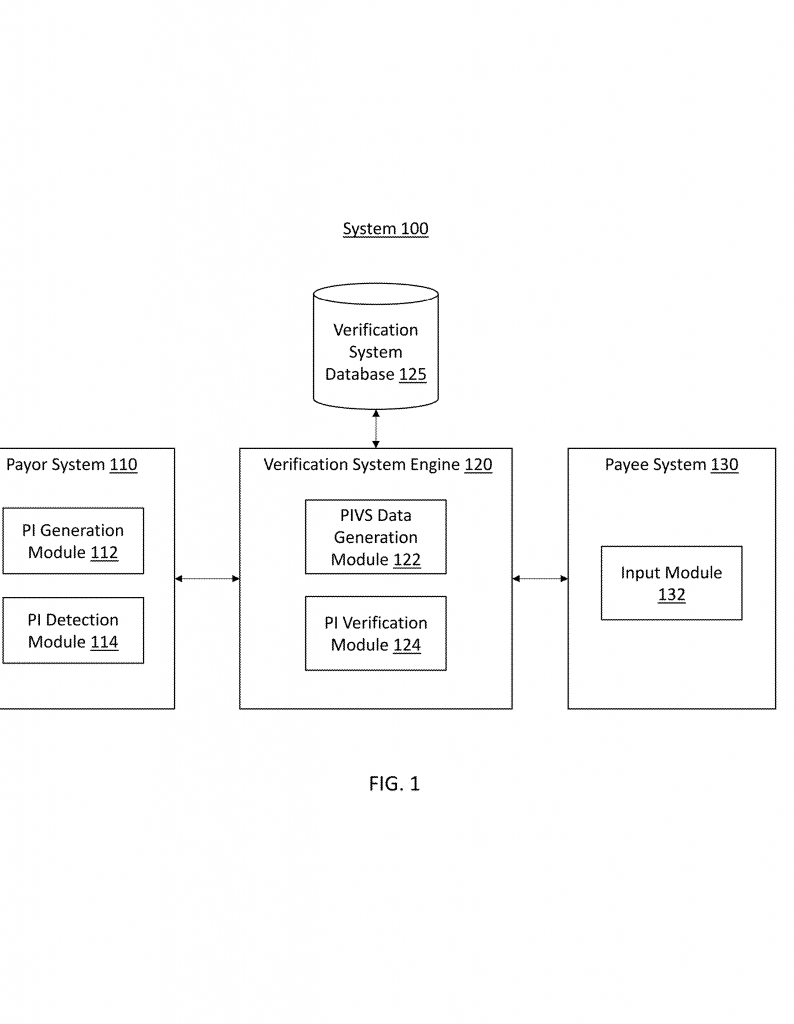

This new invention is a big step forward in payment security. It’s built around a special engine—called a Payment Instrument Verification System (PIVS)—that creates a unique fingerprint for each payment. Here’s how it works in simple words:

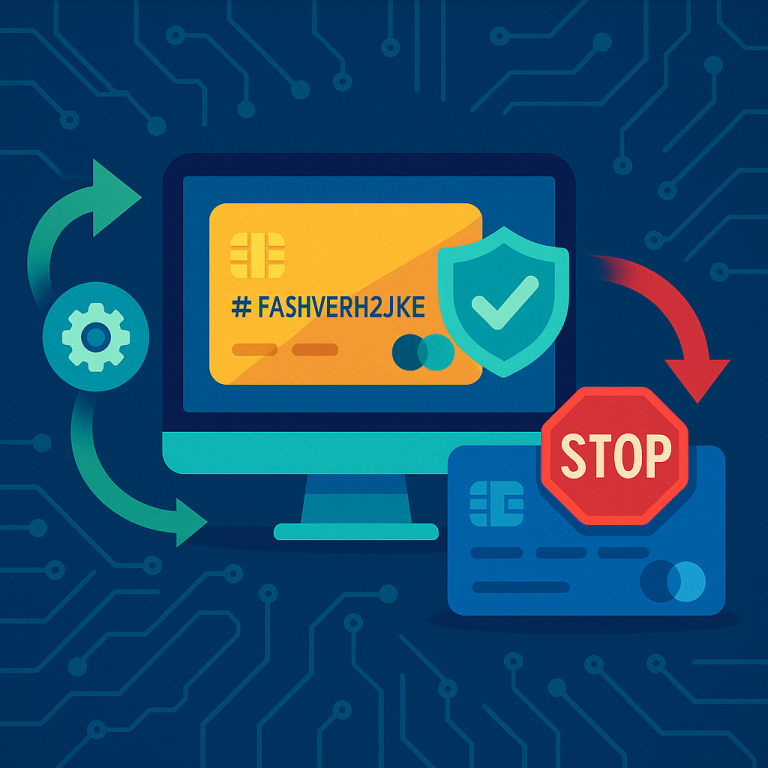

When someone (the payor) wants to make a payment—like writing a check or sending a digital draft—the system takes all the information about that payment. This can include the payor’s name, the payee’s name, the amount, date, account numbers, and even a note or memo. It puts this information through a hash function, which scrambles it into a long, unique string of letters and numbers. This is the “PIVS data.” Think of it like a secret code that only fits this one payment. If you change even one detail, the code changes too.

For even more safety, the system can use a private key that belongs only to the payor. This key adds an extra layer, making it almost impossible for anyone else to copy or fake the payment’s code. The PIVS data, and all the payment details, are saved in a safe database. This database links each code to its matching payment.

When the payee (the person or business getting the money) wants to cash the check or receive the payment, they send their copy of the details—like the code from the check, the amount, and the date—back to the system. The engine checks this new information against what’s in the database. If everything matches, the payment is good, and the money can move. If something doesn’t fit, the system blocks the payment right away. No waiting days or weeks. Both the payor and payee get quick feedback, so they know if the payment is safe.

The invention can work with paper checks, digital checks, digital negotiable instruments, and digital drafts. For paper checks, the system can even add the unique code or a QR code right onto the check—either printed or as an electronic image. If a payee scans the QR code, it reveals the code and makes it easy to check the payment’s authenticity. If there’s a problem, the system can ask for a photo of the check. It uses smart tools to read details from the image and double-check everything.

For digital payments, the system works even faster. It can use digital signatures, public keys, and other details to make sure the payment is real and hasn’t been changed. The system is designed to be quick—it can check payments in real time, often in less than a second. And because it uses smart database searches, it doesn’t slow down, even if there are millions of payments to check.

What makes this invention special is how it brings together many powerful ideas. It uses hash functions and private keys to make each payment unique. It stores everything in a secure database, linking each code to its payment. It works with both old and new types of payments, from paper checks to digital ledgers. And it gives instant feedback—letting people know right away if a payment is safe or if something’s wrong.

It also helps stop fraud before money moves. If a criminal tries to use a fake check or a copied digital payment, the system will notice and block it. The payor gets a warning, so they know someone tried to use their details. This helps everyone react faster, stopping more crime and keeping money safe.

The invention is also flexible. Banks, businesses, or even people can use it through apps, web pages, or connected devices. It can connect with other systems using APIs, making it easy to fit into today’s payment networks. And because it’s designed to work fast, it doesn’t slow down the process. In fact, it can help banks and businesses save money by catching fraud early and reducing the need for slow, manual checks.

By combining smart science with simple steps, this invention gives everyone a better way to trust payments. It’s like having a security guard for every check, transfer, or digital draft—one who never sleeps and always checks every detail.

Conclusion

The world needs safer, faster, and smarter ways to check if payments are real. This new patent application shows how to do it—using unique codes, secure databases, and quick checks for every transaction. Whether you use paper checks or the latest digital payments, this system can help stop fraud, save time, and build trust. It’s a leap forward that makes paying and getting paid easier, safer, and more certain for everyone.

Click here https://ppubs.uspto.gov/pubwebapp/ and search 20250335921.