SYSTEMS AND METHODS FOR GENERATING A CONSUMER PROFILE REPORT

Invented by Hewitt, JR.; James Franklin

Empowering Consumer Profiling: Next-Gen Systems for Transaction-Driven Insights with Full Consumer Consent

Introduction: Why Modern Consumer Profiling Needs a Paradigm Shift

For years, merchants and marketers have relied on opaque or one-directional data gathering to inform targeted campaigns, but consumers have been left out of the loop, often having little or no control over how their transaction histories are used. The result? Decreased trust, compliance headaches, and billions lost to inefficient targeting and privacy missteps. However, a new patent-pending system for generating consumer profile reports—where the consumer explicitly selects which transaction data gets included—promises to transform this crucial facet of commerce.

In this deep dive, I’ll explain how this system works, why it’s a breakthrough for both consumers and businesses, explore real-world business applications, and provide market analysis using credible data. I’ll also address top questions from technology evaluators and strategic buyers—and show how our firm is driving digital PR and thought leadership across the fintech IP landscape.

Restatement & Summary of the Invention

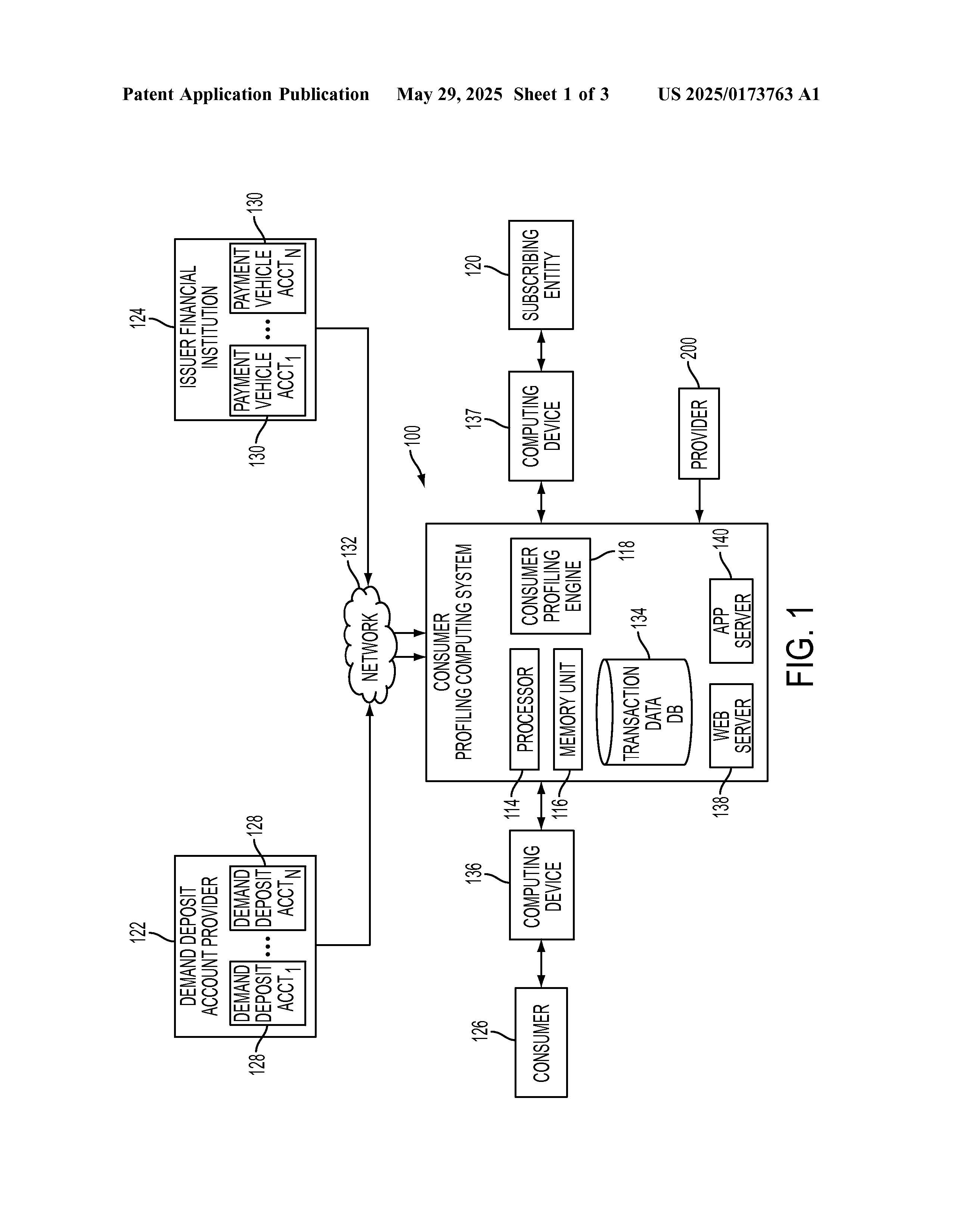

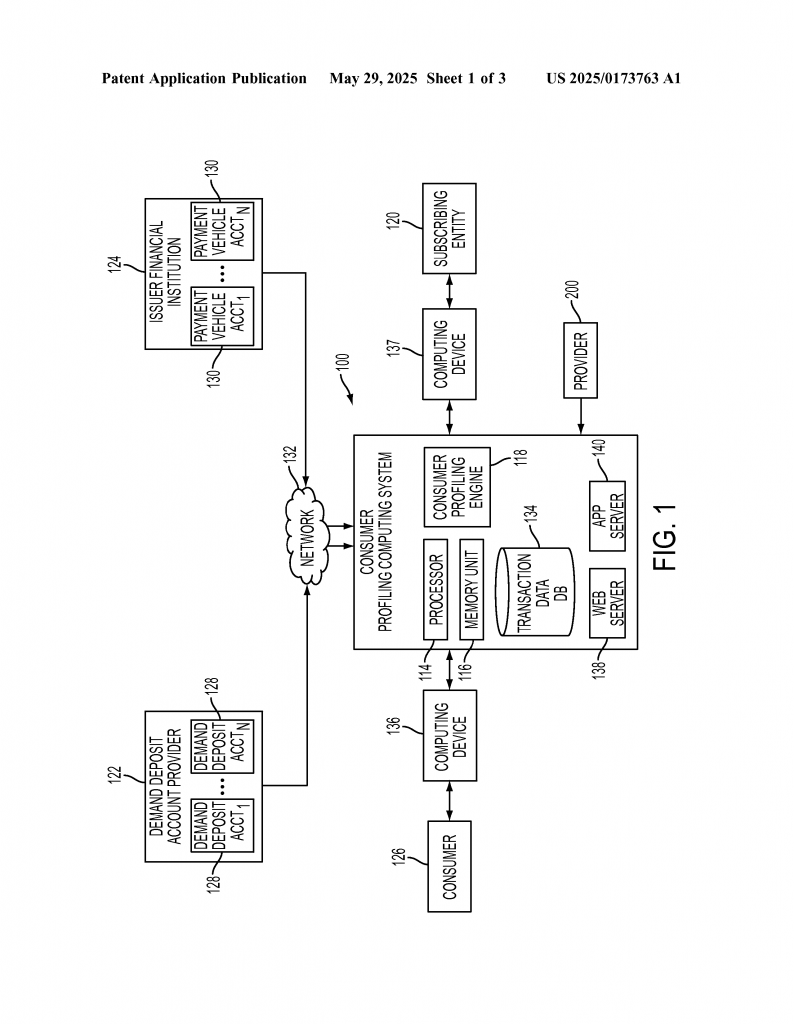

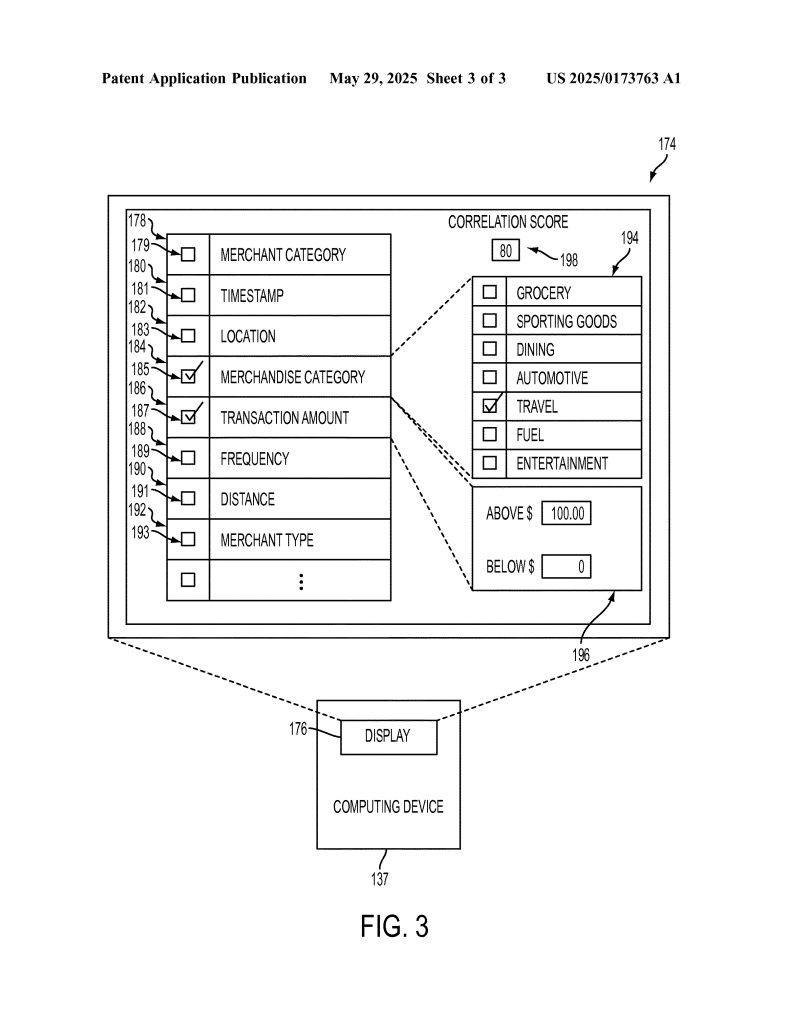

At its core, the system enables a consumer profile computing platform to securely receive, authenticate, and synthesize transaction data from multiple sources—such as a credit/debit account and demand deposit account (e.g., checking, savings)—after obtaining consumer consent. The consumer is given granular, intuitive control (via a user interface) to select which transactions or attributes to include in a profile report. This authenticated, consumer-approved profile is then generated (often with selected filters/parameters from a subscribing entity such as a marketer, agency, or offering partner) and returned as a certified profile report for targeted engagements, loyalty offers, or decision support.

| Component | Function | Benefit |

|---|---|---|

| Multi-Source Transaction Aggregation | Receives and stores data from various financial institutions | Holistic & accurate consumer insights |

| Consumer Selection Controls | User interface for choosing data granularity/inclusion | Privacy by design; enhanced trust & compliance |

| Parameter Selection by Subscriber | Subscribing entities define report filters (merchant, amount, time, etc.) | Highly tailored and relevant marketing/offerings |

| Transaction Data Authentication & Certification | Ensures data authenticity, provenance, and security | Prevents fraud, increases value of the data |

| Correlation Scoring | Matches consumers to defined criteria for effective targeting | Optimizes campaign ROIs, reduces waste |

Main Business Applications

While the system is a technical feat, its greatest value lies in the broad range of markets and problems it addresses. Here’s how different industries and stakeholders benefit:

- Retailers & E-Commerce: Hyper-targeted promotions, loyalty offer customization, segment-based advertising with ironclad data provenance.

- Financial Institutions: Enhanced customer profiling, cross-sell/up-sell opportunities, offer management with granular customer consent.

- FinTech/MarTech Providers: Turnkey APIs or platforms for privacy-centric consumer profiling, integrated into existing CRM, DMP, or CDP solutions.

- Analytics and Credit Bureaus: Consent-driven data enrichment for alternative credit scoring or account insights, helping underbanked populations.

- Healthcare, Insurance, and Regulated Domains: HIPAA/GLBA-compliant profiling by allowing customers to redact sensitive purchases while still creating valuable financial behavior profiles.

- Consumer Credit/Alternative Lending: Basis for advanced underwriting, fraud prevention, and dynamic offer pre-qualification.

- Consumer Empowerment Apps: Tools for personal finance management, digital ID, and monetization of one’s own data for offers or cashbacks.

Sample Workflow

- Consumer links external bank accounts and selects which transactions/categories to share.

- Merchant (subscriber) requests report on criteria (e.g., “Show me all users who spent over $300 at electronics stores in Q1”).

- System generates certified, privacy-filtered report, ranks users via correlation scores.

- Only relevant, interested consumers receive highly relevant outreach/offers.

Market Size & Opportunity Analysis

TAM/SAM/SOM Breakdown

The addressable market for authentic, consumer-controlled transaction profiling is both huge and rapidly growing, intersecting with several sectors:

- Consumer Data Platforms & Personalization Martech

- Open Banking & Consumer Financial Data Access

- Direct-to-Consumer Digital Advertising

- Loyalty & Customer Engagement Platforms

- Alternative Credit Scoring and Underwriting

- PrivacyTech and Consumer Data Monetization

Market Size Table

| Segment | 2023 (USD Bn) | 2027 (USD Bn; Forecast) | CAGR | TAM/SAM Estimate |

|---|---|---|---|---|

| Personalization Martech & CDP | $11.3 | $22.1 | 18.8% | TAM |

| Open Banking FinTech Software | $7.5 | $16.7 | 22.5% | SAM (US/EU/UK) |

| Data Monetization & PrivacyTech | $2.0 | $5.9 | 29.1% | SAM |

| Digital Advertising (US—Direct) | $175 | $260 | 10.3% | TAM (Relevant sub-segment) |

| Loyalty Management Platforms | $5.3 | $9.5 | 15.6% | SAM |

| Alternative Credit/Identity (US) | $1.7 | $3.6 | 21.0% | SAM |

The total addressable market (TAM) for platforms enabling authenticated, participatory consumer profiling well exceeds $25 billion globally, with a directly serviceable addressable market (SAM) encompassing $8-15B depending on integration scope and target industry.

Notable Proof Points & Trends

- Open Banking regulations (such as in EU PSD2, UK OBIE, US CCPA) require explicit consumer consent to use financial data for targeting or risk/loan assessing processes.

- Major brands are increasing spend on privacy-compliant personalization as third-party cookies deprecate and as scrutiny on unconsented data usage intensifies.

- Alternative credit scoring and embedded finance are seeing rapid adoption, but lack widespread consumer trust—solved directly by giving the consumer data curation control.

Product Deep-Dive: Common Stakeholder Questions

What types of data does the system aggregate? Is full control really possible?

The platform collects:

- Transaction data from credit, debit, prepaid, investment, and deposit accounts

- Metadata such as merchant ID, merchant type, geo-location, timestamp, amount, frequency

- Additional data such as loyalty program participation may be optionally linked

Control is at multiple levels: users can approve every transaction, exclude “sensitive categories” (e.g., health, political, religious), define parameters by merchant/type/date, and can set future preferences (opt-in/opt-out by default).

How is consumer privacy protected? What about regulatory compliance?

- Opt-in & “purpose-limited” profiling in line with CCPA, GDPR, GLBA, and PSD2

- Audit trails and data provenance for every reported transaction, allowing “right to be forgotten” and retraction

- Authentication certificate on every profile, so marketers only use data that’s certified as consumer-approved

- Fine-grained redaction (e.g., masking of individual transactions or categories)

If I’m a retailer, how do I use this data?

- Create highly targeted campaigns (“Show offers to shoppers who spent $500+ at sporting goods stores between March–May in Boston”)

- Improve conversion rates from 1% to 7% or greater* (case studies from direct-to-card-linked offers suggest 5-8x lift with actual transaction data vs. modeled)

- Add new value to loyalty programs by presenting personalized offers only to eligible consumers

*Exact rate lift depends on industry/vertical and campaign execution.

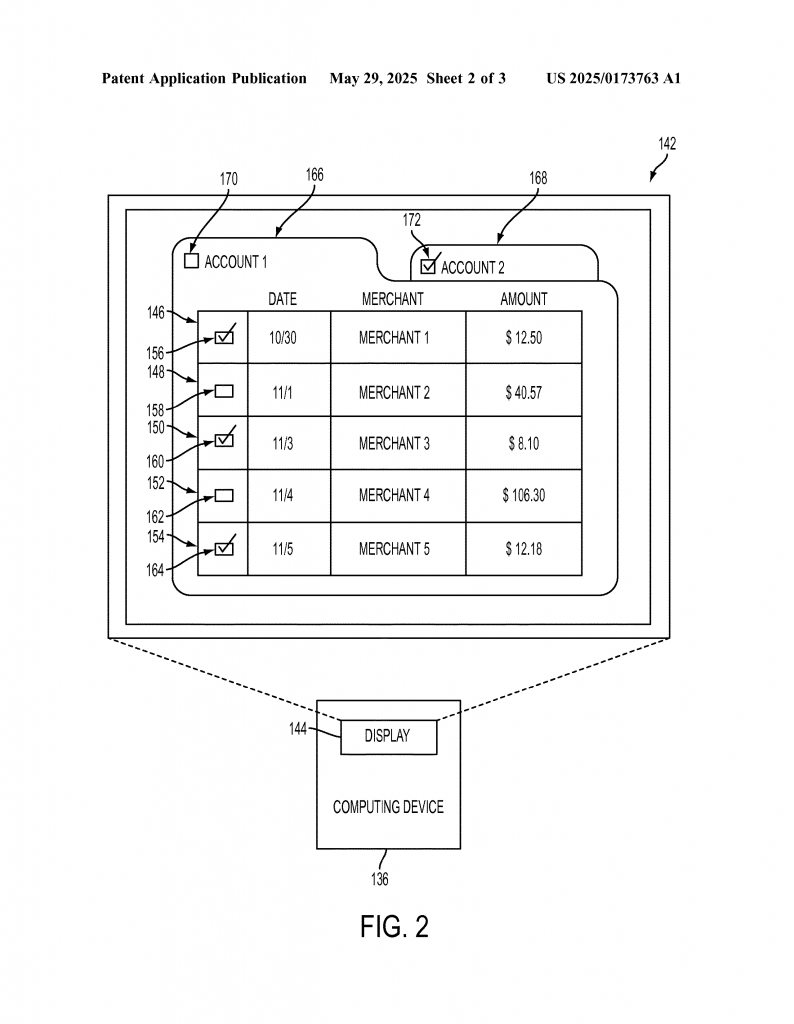

What does the user experience look like for the consumer?

- Intuitive dashboard (web/mobile) showing bank/card sources and transaction feeds

- Checkboxes or toggles for easy selection of which transactions/categories/merchants are included

- If an offer/promotion is received, the consumer can see which data was used to target them

- “Monetize my data” tool allows participation in offers for cash/reward if sharing selected data with brands

Is the system integrable with existing fintech/marketing stacks?

- Yes – all major CRM, CDP, and MarTech platforms can consume the reports via API or SFTP

- SDKs for mobile/online banking apps, loyalty apps, account aggregators

- Supports Open Banking API standards (FAPI, PSD2) for seamless plug-in

Technical Overview for Product Teams

- Enterprise-grade security with authentication/tokenization at rest and in transit

- Configurable certification module for profile report authenticity (digital signature, PKI, or blockchain option)

- Aggregate, compute, and return scored profiles at scale (millions of users per day)

- Consent logs, versioned data, and audit support for compliance and dispute resolution

Digital PR & Thought Leadership: Spreading the Word

At FintechIP Solutions, PLLC, we proactively partner with leading media outlets, research organizations, and industry analysts to expand awareness of consumer-first personalization innovations. Our commentary on privacy-compliant consumer data sharing, payment ecosystem trends, and patents for consumer data controls has been cited in:

Have a fintech or data-regulated innovation to protect? Contact us for a free analysis, IP audit, or strategic partnership discussion—our attorneys and engineers are fluent in the language of modern data-driven commerce.

Conclusion: A New Standard for Trust and Value in Consumer Data

As the world moves to consumer-first, authenticated, and privacy-respecting data platforms, those who control the rails—technically and legally—will win both customer trust and market share. The patented system described here not only addresses the technical necessity for authenticated, granular, and consumer-controlled profiling, but also provides the scalable infrastructure required for tomorrow’s marketing and fintech ecosystem.

If your business, technology stack, or data aggregation service is touching consumer payment data, now is the time to architect with both compliance and innovation in mind.

Ready to unlock the value of certified, consumer-controlled transaction data? Reach out to FintechIP Solutions, PLLC—we are your partners from ideation to patent issuance, licensing, and commercial success.

Click here and search 20250173763.